NFT, Art and Royalties

A Space Full of Promises

The NFT market experienced an euphoric period in 2021, which allowed for global testing of its potential and promises. And there have been many promises:

- “True ownership”

- Data immortality

- Censorship-resistant

- Paradigm shift in the art world

- Artist valuation

- Lifetime royalties

These promises, which are goals, were perhaps perceived as givens, and many were disappointed with their Web3 experience. Let’s be honest: the market was too young to fulfill all of these.

Yet, here we are in mid-2023, and the NFT ecosystem continues to advance every day, one step at a time, sometimes under difficult conditions. For example, the NFT standard for royalties (EIP-2981) has been increasingly used, but Opensea was slow to integrate it… then a war between NFT marketplaces erupted. Amid the bidding war of initiatives aimed at optimizing transaction fees as much as possible, one move unanimously angered the artist community: the removal of “creators’ fees” or royalties. Faced with the pressure, the marketplaces partially backtracked and left the choice to users whether or not to pay royalties.

With the arrival of Ordinals, the promise of immortality and censorship resistance is fulfilled. The debate over block size has long been resolved by the Bitcoin community, so the question now is which masterpiece deserves to exist forever.

However, the naive atmosphere of 2018-2019 is gone. The NFT market is maturing, and so is the digital art market. Despite some objections, promises continue to be fulfilled, and more are yet to come, particularly thanks to account abstraction. But before we get too carried away with the future, let’s take a comprehensive look at the art market, and more specifically, the current state of royalties for artists.

Methodology

For this report, we used only on-chain transactions of ERC-721 tokens on Ethereum. Of all the NFT transfers, a significant portion cannot be considered as an integral part of the market (tests, bots, wash-trading, etc.) and therefore, have been removed from this report.

From April 2018 to July 2023, 398 individual Smart Contracts on Ethereum were taken into account for this study, out of a total of 10,915 Smart Contracts tracked. Here are the main marketplaces collections observed, :

Royalties have been calculated based on sales in the secondary market and vary depending on the fees taken by the marketplaces for the sales that took place on them. To find out what the artist received, the percentage taken by the marketplace was deducted from the amount of transaction fees, excluding gas fees.

Here are the percentages taken by each marketplace on the secondary market:

- SuperRare: 3%

- Opensea: 2.5%

- Known Origin: 2.5%

- Makersplace: 2.5%

- Foundation: 5%

- Rarible: 1%

Note that starting from January 2023, royalties have become optional on Opensea and other marketplaces.

Art and NFT : Global Statistics

Global statistics of the NFT Art market

Like the rest of the NFT market, August 2021 marked a turning point in the art sector. The peak is particularly explained by Art Blocks, which generated a sales volume of $657 million, representing 77% of the total volume for August 2021. This percentage has gradually decreased to make room for individual creators’ smart contracts.

The sale of Beeple’s work in February 2021 was as much a trigger for the NFT “bull market” as the war in Ukraine in March 2022 was an end marker. Since then, volumes have decreased despite the proliferation of art-focused marketplaces and the entry of traditional auction houses.

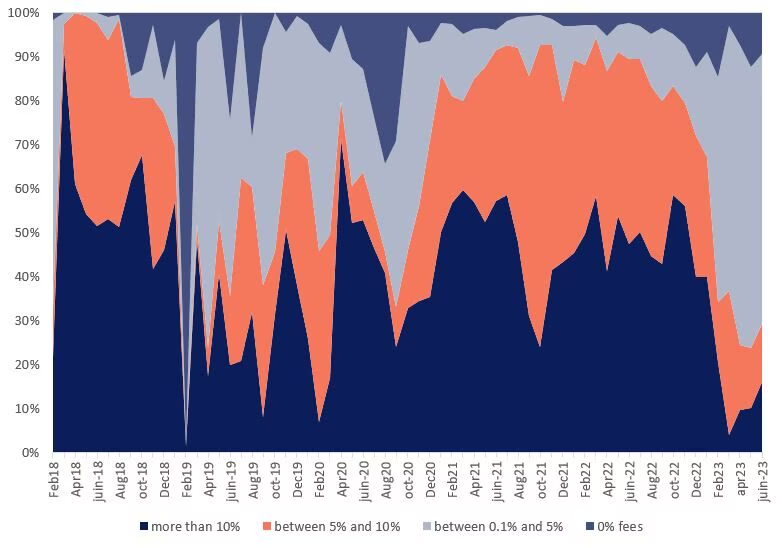

Art Collectors Are For NFT Royalties

Share of the fees paid by NFT collectors through time

The issue of royalties has always been central to the NFT ecosystem. For the art market, many worried voices have risen at the end of 2022 because of Blur’s relentlessness to remove royalties from sales.

Collateral victim, the art market has not been spared by this war between marketplace and the number of sales with fees worth less than 5% the sale price has radically increased to reach 70% of the volume in April 2023. By leaving the fees and royalties optional for collectors, it would seem that Opensea has returned the hot potato of responsibility directly to users, who have not deprived themselves of paying less fees.

But despite this shock, the percentage of the number of transactions at 0% royalties has not changed much since the beginning of 2023. It seems that the artistic sector has been heard by collectors: even if it is time to save money because of the bear market, support for artists remains here.

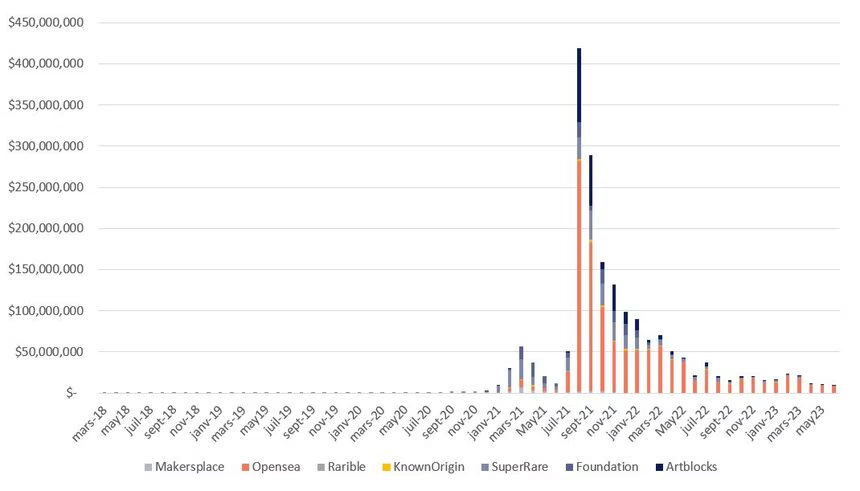

NFT Marketplaces volume

Tota USD volume per NFT marketplaces

Sales volume was concentrated on the first NFT art marketplaces such as SuperRare, Known Origin or Makerplaces until August 2021. The arrival of Artblocks and Foundation then opened the door to a larger secondary market that took place on Opensea. In addition to these two new art marketplaces, the number of individual smart contracts experienced a strong growth in 2021, further accentuating the sales volume on Opensea.

The total USD volume of each marketplace is:

- Opensea: $1,165,440,863

- SuperRare: $283,058,027

- ArtBlocks: $247,670,326

- Foundation: $138,697,370

- Makerplace: $24,601,867

- Known Origin: $21,013,247

With more than one billion volumes, Opensea is undoubtedly the marketplace that has the most volume on the primary and secondary market combined. This is explained in particular by the prices on the secondary market which soared in 2021 but also the increase in personal smart contracts since that period. In the absence of an internal marketplace, the volume was therefore concentrated on Opensea. Despite a low number of sales, SuperRare occupies the 2nd place with $283,058,027 in volume, confirming its place as the leading marketplace specializing in art.

With an average monthly volume of $2,102,499 for the first half of 2023, the NFT art market has evolved dramatically since 2018. Indeed, recall that this average was $981 in 2018, $ 6,581 in 2019 and $ 151,321 in 2020. In 2021 and 2022, it was $15,649,496 and $10,075,242 respectively.

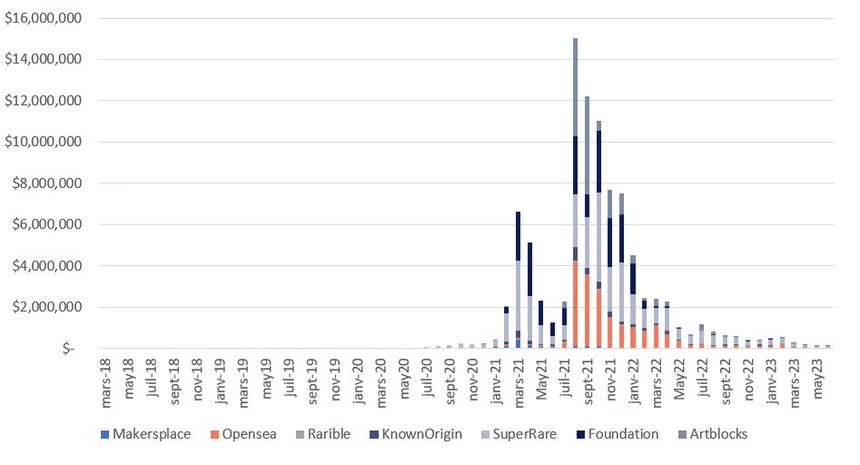

Fees Earned by NFT Marketplace

Fees earned by NFT marketplace through time

Combining the fees collected on the primary and secondary market, the total volume of the 7 main marketplaces represents $93,858,531. SuperRare is the marketplace that represents the largest volume as of July 1, 2023 with $32,732,362 then Foundation with $21,865,617 and Opensea with $19,276,549.

All time fees earned by NFT marketplaces

The fees collected are mainly concentrated on artistic marketplaces including the secondary market.

The volume on Opensea concerns individual art collections that did not have a dedicated marketplace to sell their works. Rarible, despite its low fees, recovered $237,375 in market fees.

Representing 79% of the costs recovered, artistic marketplaces dominate the artistic royalty market compared to more general marketplaces such as Opensea or Rarible

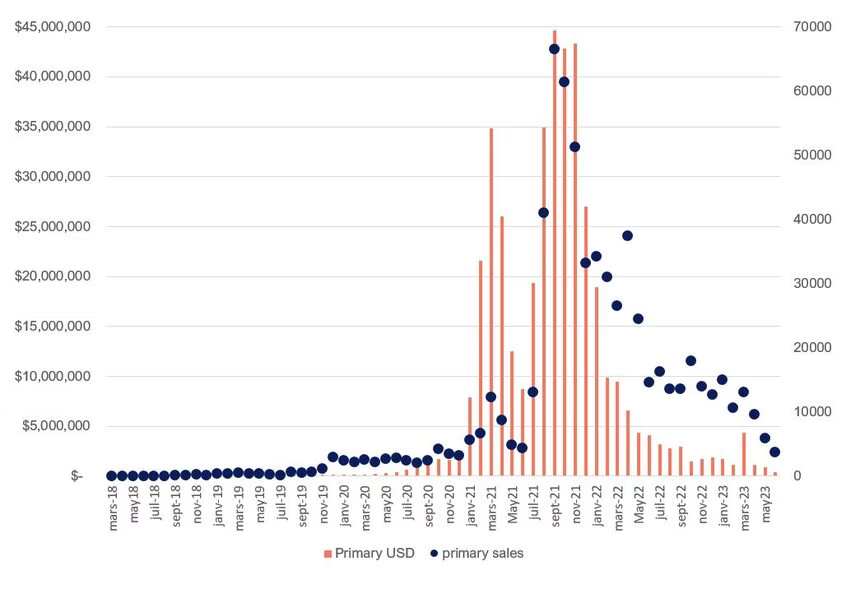

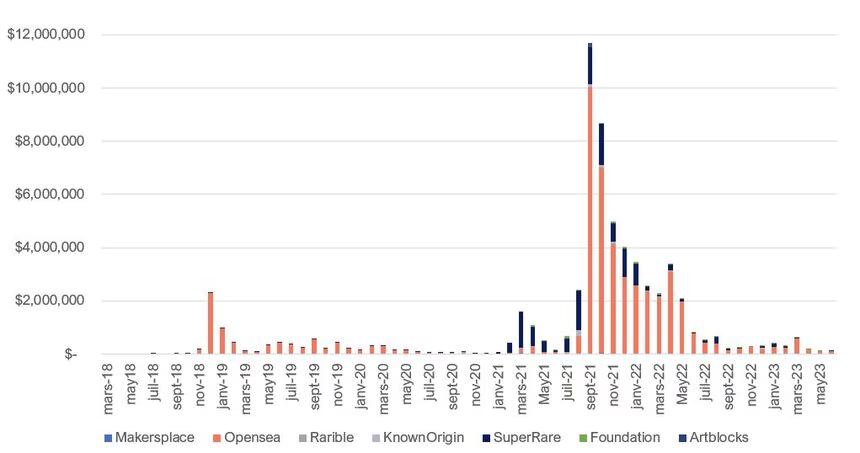

Primary Art Market

Primary sales and USD volume through time

The primary market is the preferred source of income for artists. With a total of $411,581,497 for 665,069 sales, this market that exploded in 2021 balanced in 2022 at levels higher than 2020.

This decline in sales can be explained by several factors:

- collectors prefer “safe” purchases like XCOPY or Fidenza on the secondary market

- The artists who arrived in 2021 did not stay

- The bear market makes it very difficult for individuals to buy

It is in this environment that artists, however more numerous compared to 2020, must evolve.

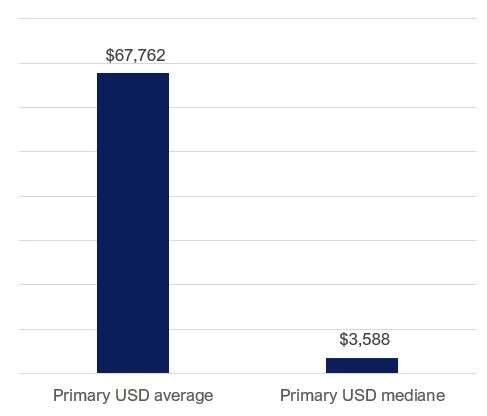

All time Primary USD – Average vs Mediane

Although the volumes for the artistic sector are high, it is nevertheless necessary to relativize the success of the artists who embark on it. Taking all the volume since 2018, the average primary market sales is $67,762 but looking at the median, it only stands at $3,588.

This disparity is explained by the volumes generated by significant primary sales of a minority of collections (Pak, Hackatao, XCOPY…) but are not representative of the majority of the market.

Artists, NFT and Royalties

Royalties earned by artists and creators through time

Combining the fees collected on the primary and secondary market, the total volume of the 7 main marketplaces represents $93,858,531. SuperRare is the marketplace that represents the largest volume as of July 1, 2023 with $32,732,362 then Foundation with $21,865,617 and Opensea with $19,276,549.

Although the primary market seems much less important than the secondary market at first glance, in reality it is the main source of income for artists and creators. But do all artists manage to sell in the same way?

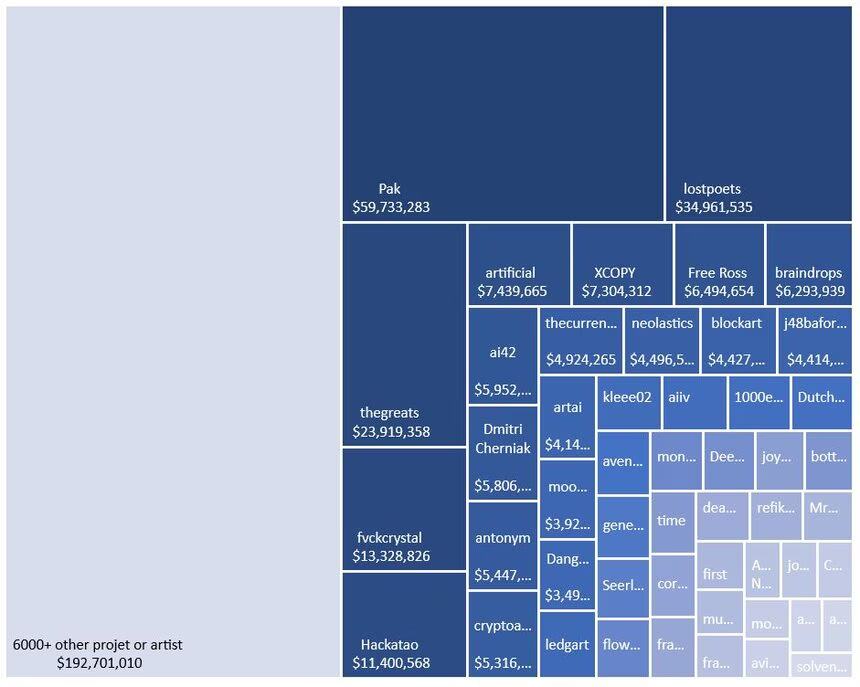

All time Primary USD Volume per project and artists

Combining all artists and artistic projects the top 100 in terms of USD volume in the primary market represent nearly 58% of the NFT art market. In the absence of Nifty Gateway’s on-chain data for the primary market, some sales like Xcopy’s Max Pain were not included in this analysis.

Is This Adoption ?

What if we had already reached our goal without knowing it? Adoption is here, with different players of all sizes wanting to try, innovate and experiment every day. The euphoria has disappeared to give way to projects that must convince, works that must surpass themselves in the face of ever more educated eyes and marketplaces that speak to ancestral auction houses…

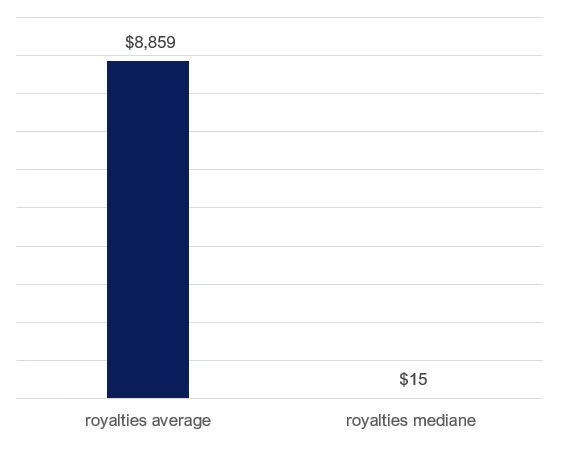

All time Royalties USD – Average vs Mediane

Looking at the USD average since 2018, the impression is given that it is possible to earn about $9000 through the secondary market but in reality, up to 50% of the 6000 artists and art projects earned only $15 in royalties. While marketplaces facilitate the visibility of artists, they must promote their work on their own.

Some excel, others less so. These complementarities create connections and form new “organized artist groups” that continue to test and experiment in chat rooms. Now that the risks are better understood every day, what will be the next step?