NFT Art Market review 2020

We are at the start of the year and our annual review for 2020 is due to be released soon, we are currently in the process of finalizing the Yearly Report, which will be our most in depth and high level report to date, covering the Ethereum on-chain NFT Market.

Many NFT sectors have shown huge developments during 2020 and one of these is in the Art Sector which experienced very strong growth over the past year. We wanted to focus on this special market where many sales records have been successively broken over the period of a few months.

This article will first present the evolution of the 4 main Art Marketplaces by returning to the phenomenon of CryptoPunks, whilst attempting to identify a trend in the Art Market that does not belong to the first two categories.

In this analysis we have considered only sales of Artworks and not the overall statistics, the costs relating to the sale as transaction costs are not counted, to try and answer the question: How has the Art Market evolved since our 2018-19 report?

NFT Art Marketplaces

First, we’ll take a look at four Art Marketplaces: Markersplace, Known Origin, Async Art and SuperRare. Blockchain Art Exchange having experienced a switch to ERC-1155 smart contracts during the year, was excluded from the results because its volume and sale prices are not complete. At the present time NonFungible.com does not support the ERC-1155 standard.

The chosen indicators are:

- Sales volume in USD

- Primary and secondary markets

- Number of unique buyers and sellers

This will give an overview of developments in the marketplace without going into the details of each sale.

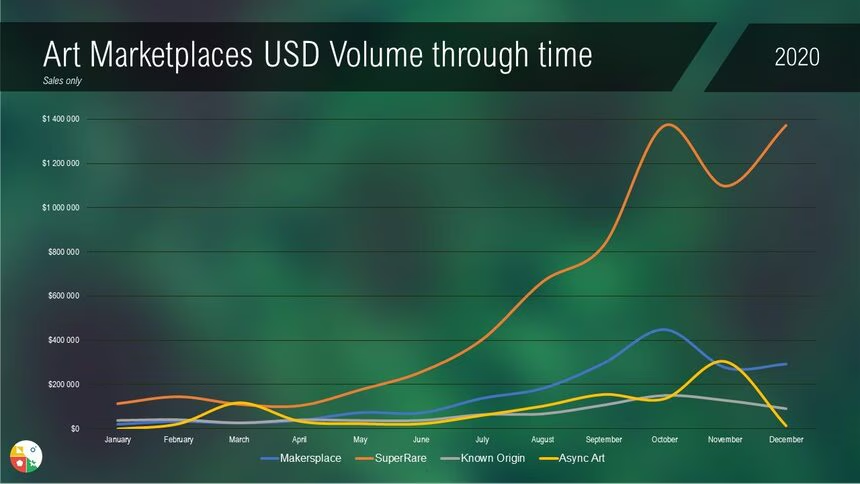

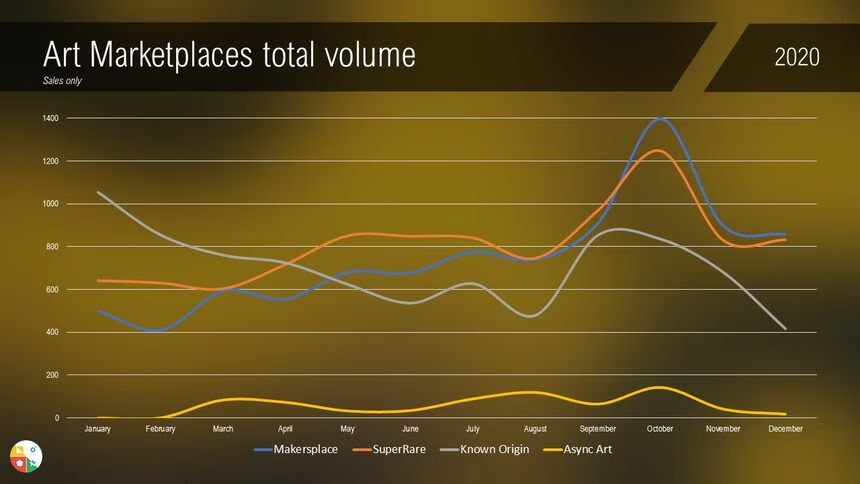

NFT Art Marketplace 2020 – USD Volume

Let’s start with the total sales volume in dollars, it emerges that SuperRare is further making its dominance known amongst the other marketplaces.

When we analyzed the overall statistics of these marketplaces last year, Known Origin was in second position, today the platform currently finds itself lagging behind.

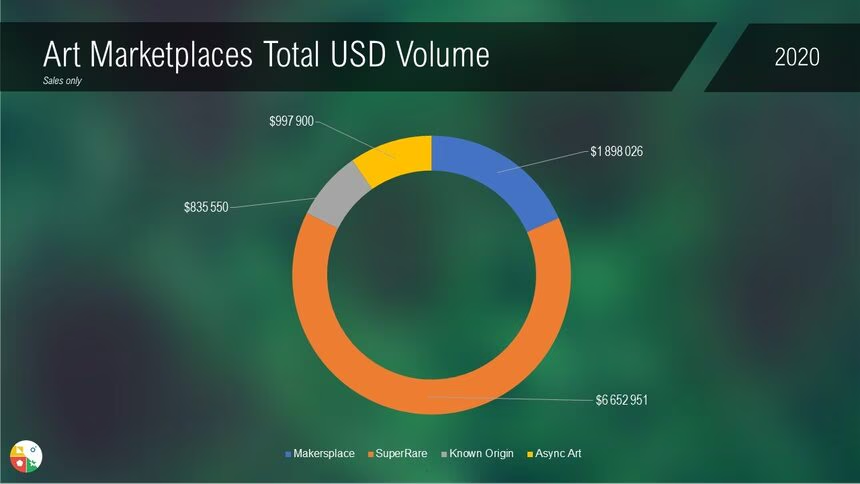

- NFT Art Marketplace 2020 – Total USD Volume *

Async Art began sales during February, their interactive works quickly found buyers!

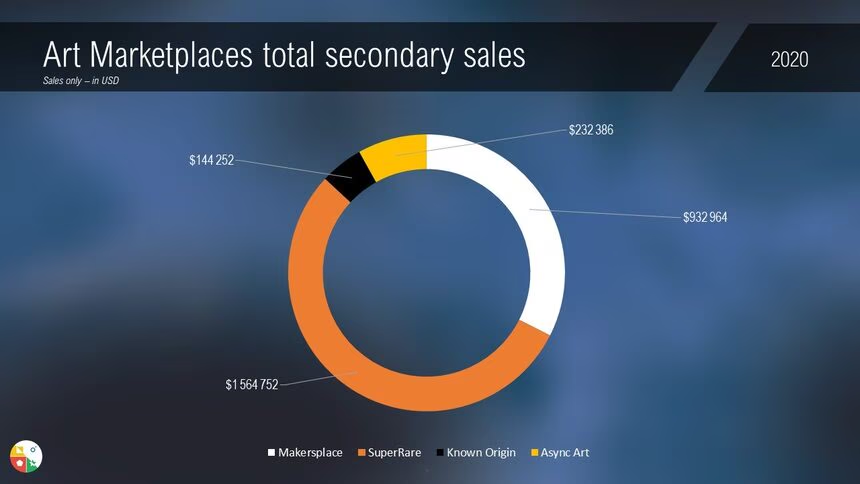

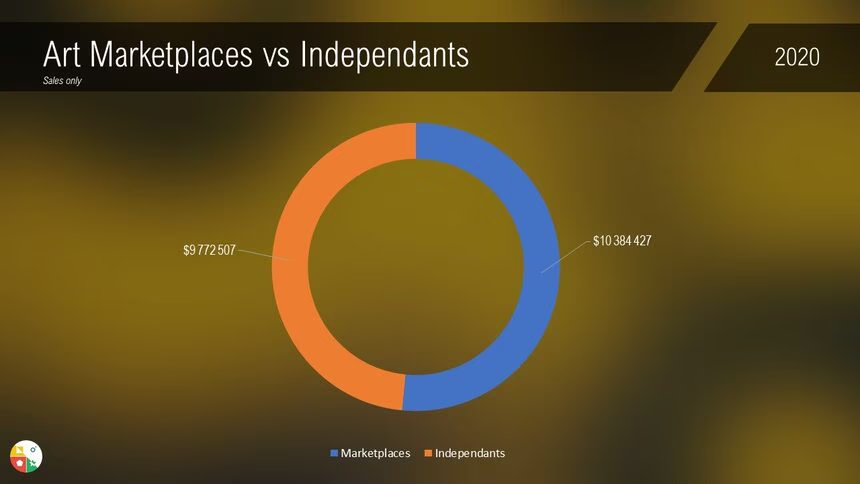

In total, the USD volume of artworks sold on these four marketplaces amounts to $10,384,427.

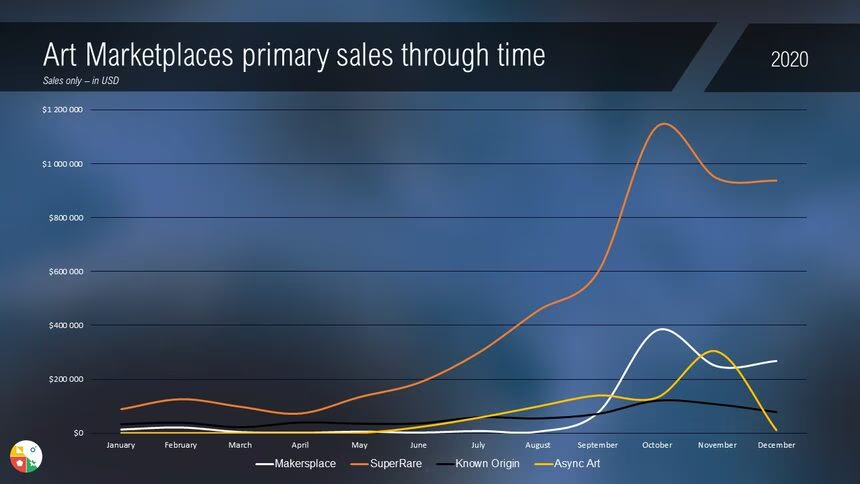

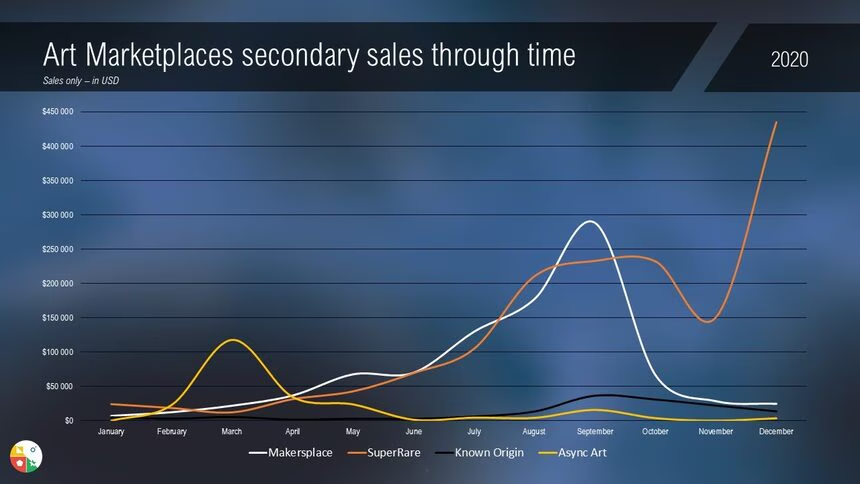

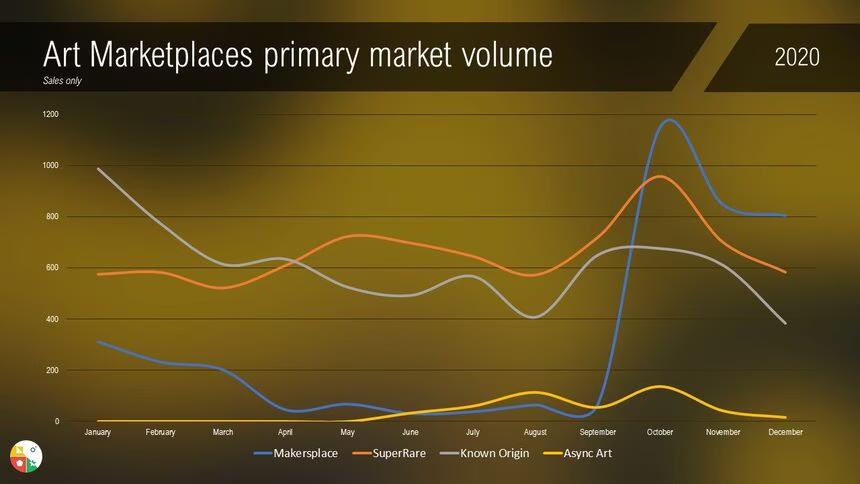

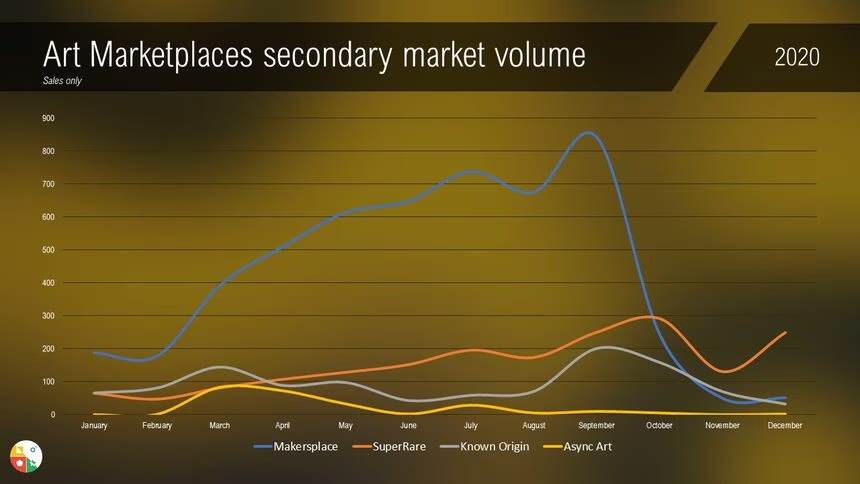

Another aspect to take into account during these sales is the split between the Primary and Secondary Markets. Last year we noticed an evolution between 2018 and 2019 but for 2020, the trend has now been confirmed: SuperRare is losing dominance in the Secondary Market.

- NFT Art Marketplace 2020 – Primary sales Volume*

- NFT Art Marketplace 2020 – Total Primary sales*

- NFT Art Marketplace 2020 – Secondary sales Volume *

- NFT Art Marketplace 2020 – Total Secondary sales*

Several times throughout the year and over several months, SuperRare was no longer leading the sellers on USD volume for the Secondary Market. However, by November, nothing could stop the growth of this leader.

Overall, the Primary Market is worth **$7,510,073 compared to a secondary market worth $2,874,353. **

So far, no marketplace seemed to be able to compete with SuperRare in terms of USD volume but by the end of the Summer an upwards trend for Makersplace is apparent with the platform exhibiting more bullishness than the other two.

Even though Makersplace only represents 13% of the Primary Market, achieving 33% of the entire Secondary Market is a major change from last year! The arrival of Jose Delbo in July seems to have had a big impact on the platform: from September a “flippening” took place, thus increasing the USD volume of the Primary Market to the detriment of the Secondary Market.

Even if in terms of USD the distribution of market sales seems clear, this data must nevertheless be cross referenced with two other factors: the number of sales of the work and the number of unique buyers / sellers.

SuperRare experienced rather stable growth over the year in both the Primary and Secondary Markets but it was with Makersplace where significant events took place for the platform!

Be it Known Origin or Makersplace, both were hit hard by the high transaction costs which plagued the Ethereum network throughout 2020. The direct consequence was a drag for artists who then saw these platforms as an affordable way to sell artworks at a low price.

However, this did not stop sales on the Secondary Market despite a low volume in USD generated during the year. that was until September when Makersplace was able to welcome the arrival of collaborations between well-known artists on its platform, giving new life to the volume of sales in the Primary Market!

The stability of SuperRare can be explained by the available means and wealth artists and buyers had on the platform, for whom high transaction fees were not a serious hindrance to making a transaction.

In total, there were 27,890 sales on the four market places, Aysnc Art offers unique artworks which explains its low sales volume, 2020 is clearly a pivotal year for Makersplace who manages to stand up to SuperRare.

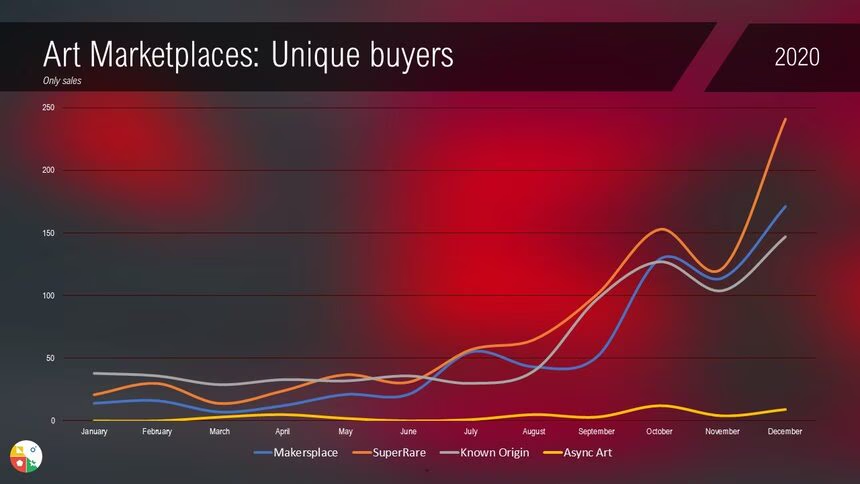

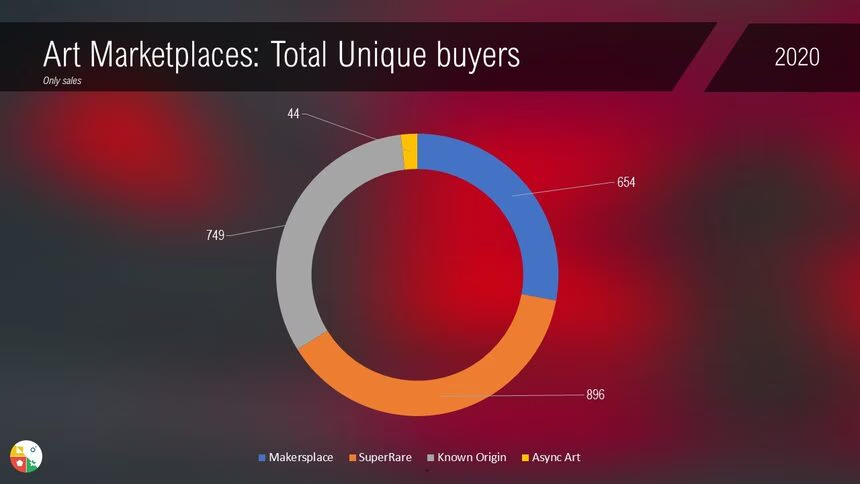

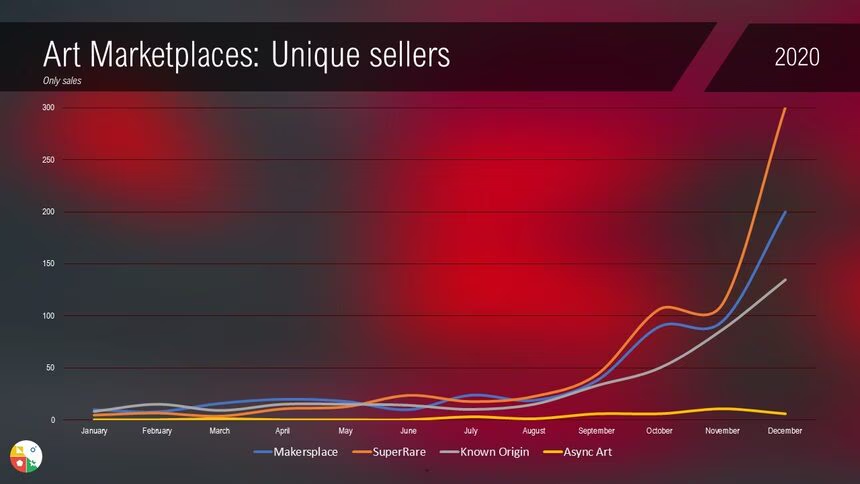

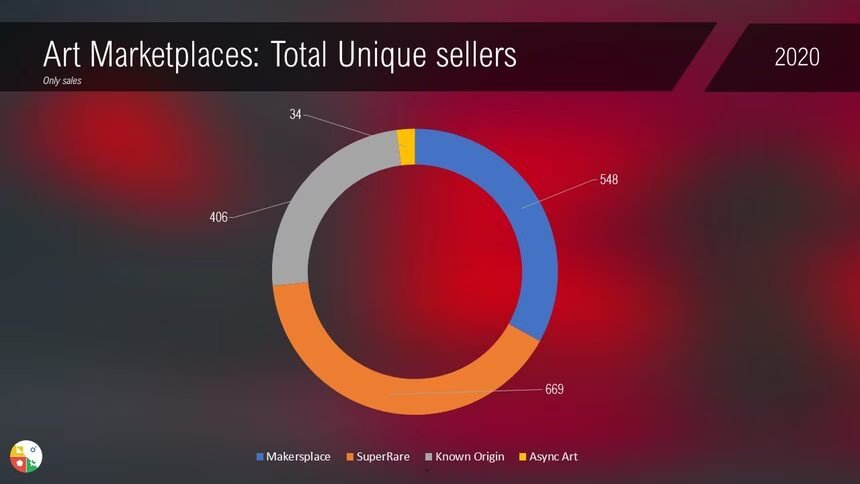

A final indicator to take into account concerns the number of unique buyers and sellers. The first thing we notice concerns the communities of Makersplace and Known Origin, until September they do not seem to have grown enormously despite a high sales volume in the first half of 2020.

But September brought its share of new arrivals and for 2020, the trend is marked by a balance between buyer and seller, showing former collectors have started to sell their pieces despite an increase in the number of buyers.

CryptoPunks

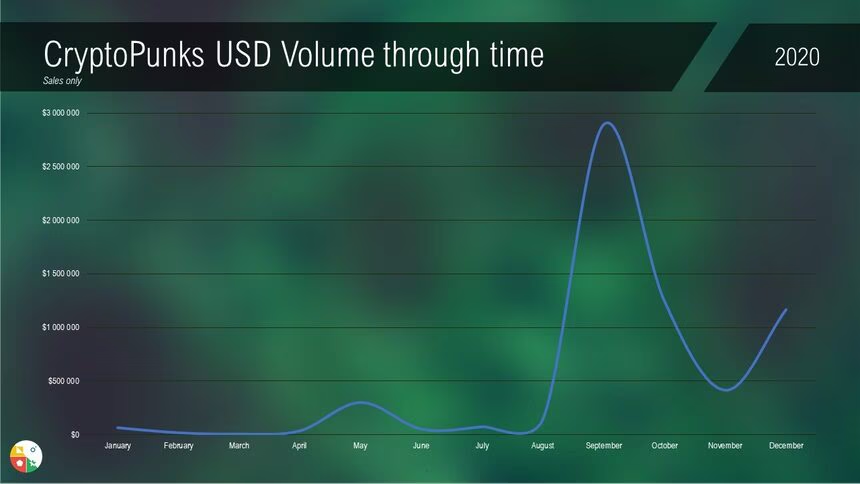

Before going into the details of different artists, let’s start with CryptoPunks and their performance over the year, it is important to point out that given the volume represented by the CryptoPunks, the project has been separated from the various graphics.

With total sales reaching $6,286,157, CryptoPunks have been a smash hit! We wrote an article retracing their evolution from their launch up until mid-December, but that didn’t account for the last fortnight of the year when the enthusiasm to buy Punks did not stop, in fact quite the contrary!

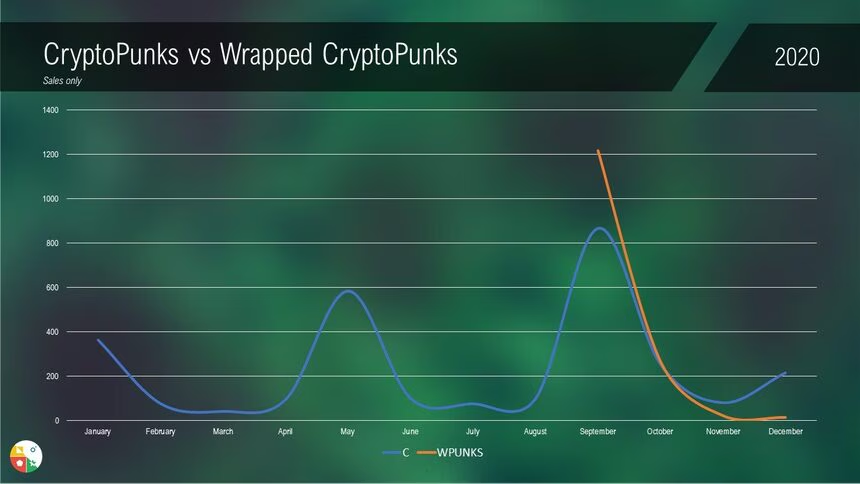

Where Punk collectors have been surprised was, without doubt, during the month of September! On one hand there was the new possibility of being able to “wrap” your CryptoPunks allowing for a much better exchange on different platforms like Opensea and seeing a total of 1,526 wrapped Punks sold generating $2,420,779.

On the other hand, and difficult to know the reasoning of the hodlers, September was marked by a completely unexpected event: **156 never-before-sold punks hit the market this month, followed by 83 more **until the end of the year, giving new life and above all new interest to the project.

The last surprise, good or bad depending on your financial capacity, is the minimum price of CryptoPunks from September. With the massive buying wave that occurred at that point, it was no longer possible to acquire Punks, first under 1 ETH, then 2… and this factor combined with the soaring Ethereum price has placed an increasingly large financial barrier for those who wanted to buy some.

Of the 4,384 punks sold in 2020, 3,471 were in the last 4 months of the year. These sales represented $5,726,146 or more than 90% volume in USD of CryptoPunks for 2020!

With a record sale for 2020 at $137,366 as of December 30 #OGs in the sector made their mark, far from thinking that this record would then go on to be shattered just a few weeks later..

But let’s stay in 2020 shall we?

The “Independants” market

Even though these four big marketplaces have led the market and alone represent the majority of volume, 2020 was a strong year of democratization for projects wishing to use Non-Fungible Tokens to express their digital art.

So we first analyzed the sales of 190 projects without distinguishing between “generative” and “non-generative” art.

Among the list are projects like Avastars, Cryptomorph, PixelChain or Codex Protocol but as we will see, what gives the greatest weight to these figures is undoubtedly all the smart contracts of individual artists.

To be able to highlight as many of these projects as possible, we have divided the volume in USD into three segments: those having generated more than $100,000, those having generated between $10,000 and $100,000 and those having generated between $5,000 and $10,000.

We then separated generative and non-generative art to achieve a better representation of artists.

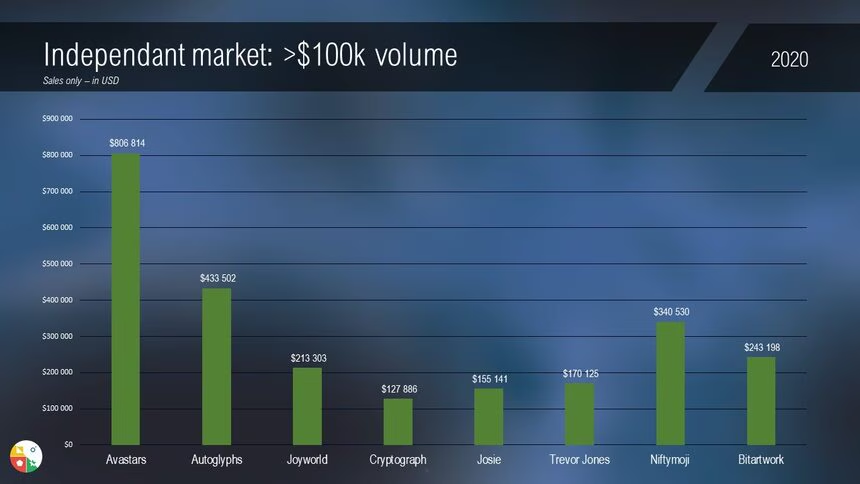

Among the 8 projects and artists that led with a volume of $2,490,497, two of them are no longer continued by their teams:** Niftymoji** and Bitartwork. While it is still possible to trade Niftymoji in various marketplaces, they are no longer used unless new developers take over.

Avastars and Autoglyphs are two projects that have founded all their value “on-chain” and what they have in common is that they are both art generated by an algorithm.

While both have all metadata as well as its graphics on-chain, Autoglyphs is the second project from Larvalabs, less known than its big brother but still having found a strong community of collectors.

Joy, Josie and Trevor Jones are three crypto-artists already well-known in the community, but this year it’s the real world that has come to know them: while a work by Josie was included in a tweet by Barack Obama, Joy got noticed by Adobe and Trevor Jones was able to sign several works with Jose Delbo, the artist best known for his work with DC Comics, Marvel Comics, and several others!

Cryptograph is a project with celebrity figures such as** Paris Hilton**,** Seth Green, Ashton Kutcher, Tom Morello, Scott Storch, Jason Momoa, Vitalik Buterin**…. The list goes on and is incredibly impressive! The celebrities and blockchain figures are featured** **as artists and all the money generated by the works sold on this platform are donated to charitable actions.

Pixelchain, with $93,389 generated for 4,058 sales, was very close to being alongside Avastars and Trevor Jones. This project allows anyone to create a pixel art work on a 32×32 (or more recently 64×64) pixel space. By leaving full freedom to anyone to express themselves and then mint an NFT, maybe a new trend is emerging for 2021?

However, we must not forget the artists who have been talked about throughout the year and who are now essential in the ecosystem today: Pascal Boyart, Hackatao, Frenetik Void, Allota Money or the controversial Maxosiris and Robness.

Generative art is also represented with projects like Colorglyphs, CryptoSkulls or CryptoMorph but it is clear that in 2020, artworks created by humans are the overwhelming majority in this ranking.

In all, these 26 projects and artists generated $711,774 over the year.

The 34 projects cited above alone represent $3,202,271 out of a total of $3,486,350 generated by sales of works by 190 projects and artists.

The 21 artists in the graph above are just the tip of the iceberg of creatives floating in the ocean of NFTs: they represent a volume of $142,412 for 3,021 works sold and it should not be forgotten that 135 other projects follow them in order to reach a total of $284,079 for 6,692 works sold.

Conclusion

There are many other metrics to showcase the health of the art-related NFT market. The one that was predominant during 2018 and 2019 was also one of the only ways for artists to find recognition: marketplaces.

But today SuperRare is reserved for wealthy wallets, Makersplace has become more expensive, Known Origin has changed little rules and Async Art seeks only interactive works with reality.

Every day new initiatives appear and even if marketplaces still occupy a dominant place in the sector, it seems that the elitism they displayed at the start did not meet a growing need among users: to create for the sake of art.

But that’s ultimately great news twice for both the ecosystem and artists around the world:

- Despite a year marked by repeatedly peaking network fees, we had valued the volume of dollars traded in 2019 at $ 559,403. For 2020, it reached $20,156,934.

- The phrase ‘do against bad luck’ seems to have been the motto for many artists who saw Non-Fungible Tokens as a way to survive repeated lock-downs

There is still a lot to do in the NFT ecosystem for it to offer the same possibilities as the real world, but the massive adoption that took place during 2020 makes us very optimistic about its future evolution and growth.

If you want to continue to explore this space with us, don’t hesitate to subscribe to our newsletter for more info to come!